Losing a job is stressful. On top of worrying about income, there’s the immediate concern about what happens to your health insurance. The last day of work often feels like a race against the clock to figure out your next move.

However, there’s a little-known feature of federal law that acts as a powerful safety net, often called the “COBRA 60-day loophole.” It’s not a shady trick or a scam, but a built-in provision that can save you from paying hundreds or even thousands of dollars in premiums for coverage you might not need.

This comprehensive guide will demystify the COBRA 60-day loophole. We’ll explain exactly what it is, how it works, and how you can use it strategically to protect yourself and your family during a job transition.

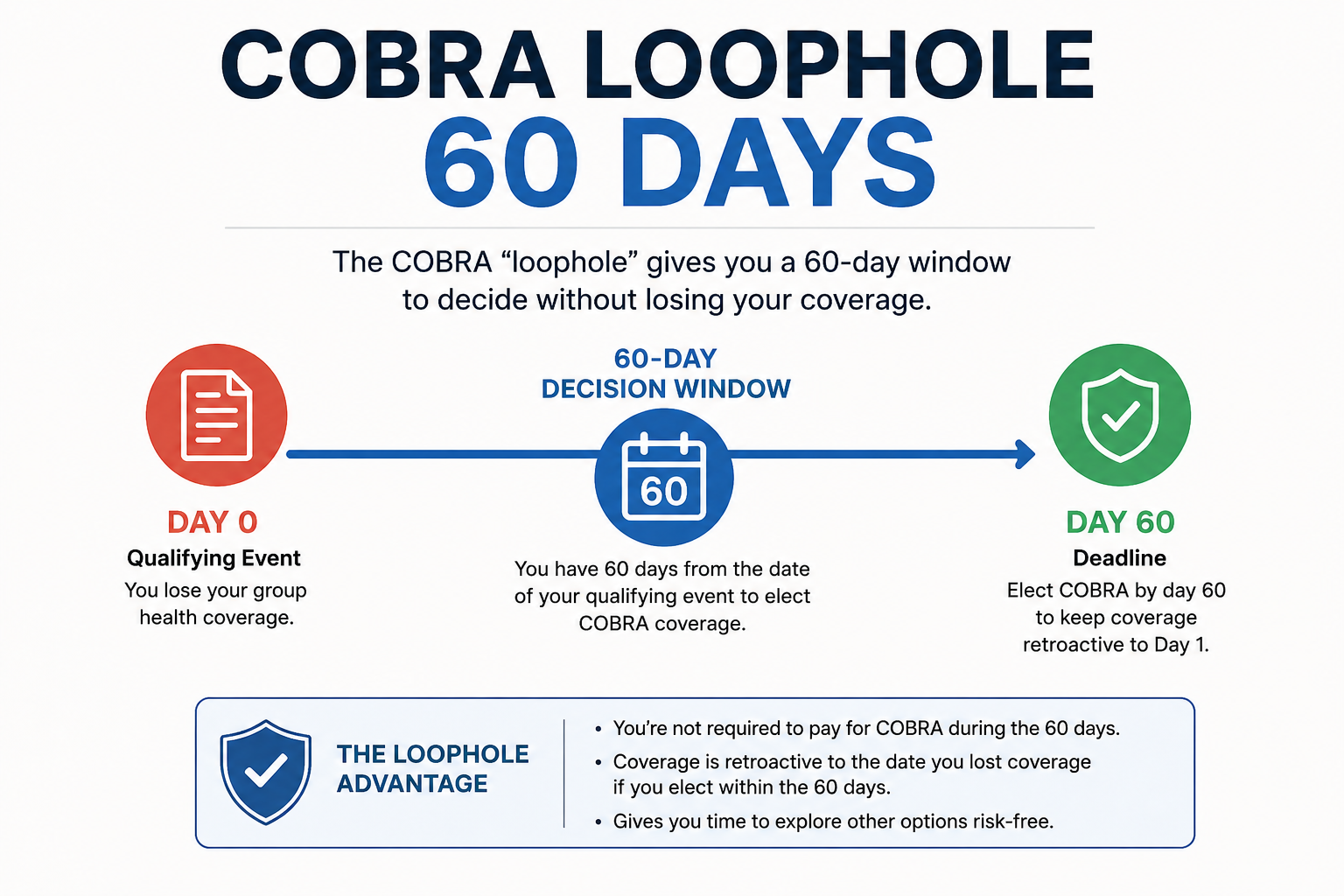

The “COBRA 60-day loophole” refers to the 60-day election period granted by the Consolidated Omnibus Budget Reconciliation Act (COBRA). This period allows you to decide whether to continue your employer-sponsored health insurance after a qualifying event like job loss.

Here’s the critical part: you don’t have to decide on your last day. You have 60 days from when you receive your COBRA election notice to make a choice. If you choose to enroll within that window, your coverage is applied retroactively back to the day you lost your original insurance.

This retroactive feature is the “loophole.” It gives you a window of time during which you are technically uninsured but have the option to activate coverage if a medical need arises. You only have to pay the back premiums if you actually use the coverage.

Understanding COBRA Fundamentals

Before diving deeper, it’s useful to understand what COBRA actually is. COBRA is not an insurance company or a new health plan. It is a federal law that gives you the right to temporarily continue your existing employer-sponsored group health plan.

When you elect COBRA, you are staying on the exact same plan you had while employed. This means you keep your doctors, your provider network, and importantly, you don’t lose any progress you’ve made toward your annual deductible.

The main difference is the cost. Your employer is no longer paying a portion of the premium. You become responsible for the full premium plus a 2% administrative fee, which can be quite expensive.

Eligibility and Key Deadlines

Understanding the timeline is crucial to using the loophole effectively. Here are the key dates to remember:

-

Qualifying Event: This is the date your employer-sponsored coverage ends. Common events include job loss, a reduction in hours, or divorce.

-

Notification Period: Your employer has 30 days to notify the plan administrator of the qualifying event. The administrator then has 14 days to send you a COBRA election notice. This means the 60-day clock may not start on your last day of work.

-

The 60-Day Election Period: This is your decision window. You have 60 days from the date you receive the election notice to decide whether to elect COBRA coverage.

-

The 45-Day Payment Grace Period: Once you elect COBRA, you have an additional 45 days to make your first premium payment. This payment is retroactive and covers the entire gap period back to the qualifying event.

This combined timeline means you could have up to 105 days from your qualifying event before any money is due.

How the COBRA 60-Day Loophole Works: A Step-by-Step Guide

The beauty of the “loophole” is its simplicity. It’s a strategic way to use the rules to your advantage without breaking any laws. Here’s how it works in practice:

-

Step 1: Receive Your COBRA Notice. Your former employer’s plan administrator sends you an election notice. This starts your 60-day clock.

-

Step 2: Do Nothing (Yet). You are not required to respond immediately. You can wait. During this time, you do not have active coverage, but you possess the option to activate it.

-

Step 3: The Wait-and-See Approach. You watch and see if you need medical care. If you stay healthy for the next 60 days and find a new job with benefits, you can let the election period expire and pay nothing for COBRA.

-

Step 4: Activate if Needed. If you have an accident, a doctor’s visit, or any medical need during the 60-day window, you can elect COBRA coverage. You will be retroactively covered back to day one.

-

Step 5: Pay the Back Premiums. To make the coverage official, you must pay the retroactive premiums within the 45-day payment grace period. This can be a large bill, but it covers the medical costs you just incurred.

Why Use the COBRA 60-Day Loophole?

Key Benefits

The primary benefit of this strategy is the potential for massive cost savings. COBRA premiums are often very high. The average monthly cost for COBRA in 2024 was $645 per month for single coverage** and **$1,852 per month for family coverage. By waiting, you avoid paying these premiums unless you actually need the coverage.

This approach provides a “no-risk” safety net. You are protected against a catastrophic medical event, but you don’t have to pay for the privilege unless the event occurs. It gives you breathing room during a transition period without the financial burden of an extra bill.

Alternative: Direct Enrollment

Of course, you can also choose to enroll in COBRA immediately. This is the simpler, more traditional route. You will pay the premiums upfront and have continuous, active coverage from day one.

This is a good option if you have ongoing medical needs, are in the middle of treatment, or simply want the peace of mind of active coverage without the administrative hassle.

Step-by-Step Guide to Using the COBRA 60-Day Loophole

If you decide the wait-and-see approach is for you, here is a checklist to help you navigate the process safely.

Checklist for Your 60-Day Window

-

Read Your COBRA Notice Carefully: Understand the exact start and end dates of your election period. The 60 days starts when you receive the notice, not when you lose coverage.

-

Compare Other Options: Don’t forget to look at other options. You have a Special Enrollment Period (SEP) to join a spouse’s plan or purchase a Marketplace plan. You have 60 days from your qualifying event to do this. Compare costs.

-

Prepare the Paperwork: Some people fill out the COBRA election form in advance and have it ready to mail or upload. This ensures you can act quickly if you need coverage.

-

Save for the Back Payment: Remember that if you use the coverage, you’ll need to pay back premiums for the entire gap. This could be two months’ worth of premiums. Budget accordingly.

-

Decide by Day 59: Don’t wait until the very last hour to make a decision. Give yourself a buffer to ensure you don’t miss the deadline.

Common Mistakes to Avoid

-

Thinking It’s a Free Trial. It’s critical to remember that you will need to pay the back premiums if you elect COBRA. It is not free insurance. You are deferring payment, not avoiding it.

-

Missing the Deadline. The 60-day window is firm. If you miss the deadline, you lose your right to COBRA coverage. There are very few exceptions to this rule.

-

Not Considering Other Options. Sometimes a Marketplace plan or a spouse’s plan is significantly cheaper than COBRA, even with subsidies. Use your Special Enrollment Period to compare all options.

Expert Tips

-

Communicate with Providers: If you need care during the gap, be upfront with your doctor’s office or hospital. Let them know you are in the COBRA decision window and that your coverage will be retroactive once you elect it. They may be willing to wait for payment.

-

Understand the First Payment: Your first COBRA payment will be larger than a normal monthly premium. It will cover the premiums for the entire time between your qualifying event and when you elected COBRA. This can be a significant chunk of change, so be prepared.

-

Keep Your Deductible: One of the biggest advantages of COBRA is that you keep your existing deductible and out-of-pocket maximum. This means you don’t have to start over with a new plan if you’ve already spent money on healthcare that year.

Real-World Example: The Loophole in Action

Let’s look at a scenario to see how this works.

Scenario: Sarah leaves her job on April 1st. Her employer’s health insurance ends that day.

April 1st: Sarah receives her COBRA election notice on April 10th. Her 60-day election period is now open until June 9th.

May 15th (Day 35): Sarah is healthy and hasn’t used any healthcare services. She is waiting to start a new job that will provide health insurance on June 1st.

May 20th (Day 40): Sarah has an accident and goes to the emergency room.

May 25th (Day 45): Sarah fills out her COBRA election form and submits it. She is now enrolled in COBRA coverage.

June 10th (Day 56): Sarah receives her COBRA bill. She has 45 days from her election date (May 25th) to pay, meaning her payment deadline is July 9th. She pays the premiums to cover April 1st through June 1st.

Result: Sarah’s COBRA coverage is retroactive to April 1st. The ER visit from May 20th is covered. She paid for 60 days of coverage but only needed it because of the accident. If she hadn’t had the accident, she could have simply not elected COBRA, started her new job on June 1st, and saved the money.

| Feature | COBRA | ACA Marketplace Plan |

|---|---|---|

| Coverage | Your exact employer plan | A new plan from the Marketplace |

| Cost | Full premium + 2% fee (often very high) | Can be subsidized, often cheaper |

| Providers | Keep your existing doctors and network | May need to find new in-network providers |

| Deductible | Keeps your existing deductible and OOP max | Starts a new deductible and OOP max |

| Enrollment | 60 days from qualifying event | 60 days from qualifying event (Special Enrollment) |

| Ideal For | Short-term gaps, ongoing treatment, keeping your plan | Longer gaps, lower cost, subsidies |

Pros and Cons of Using the COBRA 60-Day Loophole

Pros

-

Flexibility: Gives you time to decide without pressure.

-

Financial Savings: You only pay for coverage if you need it.

-

Retroactive Coverage: Protects you from a gap in coverage.

-

Keeps Your Plan: You don’t have to change doctors or plans.

Cons

-

No Active Coverage: You are technically uninsured during the waiting period.

-

Huge Back Payment: If you do need it, you’ll have to pay a large lump sum of back premiums.

-

Not a Free Trial: Some people mistake the window for free coverage, which it is not.

-

Paperwork: You must be organized to ensure you meet the deadlines and submit the correct forms.

FAQ Section

What exactly is the COBRA 60-day loophole?

It’s a feature of federal law that gives you 60 days to decide whether to continue your employer’s health insurance after a qualifying event like job loss. If you elect COBRA within those 60 days, the coverage is retroactive to the day your old plan ended.

Is the COBRA 60-day loophole legal?

Yes. It is not a loophole in the sense of a scam. It is an intended feature of the law designed to give you time to make an informed decision without a gap in coverage.

Do I have to pay for COBRA if I don’t use it?

No. If you let the 60-day election period expire and you do not enroll, you owe nothing.

What happens if I get sick during the 60-day window?

You can elect COBRA coverage at any point during the 60-day window. Once you pay the back premiums, the coverage will be retroactive, and it will cover your medical bills.

Can I change my mind about COBRA during the 60 days?

Yes, you can change your mind as many times as you want during the 60-day election period. Your decision only becomes final once the period ends or you formally enroll.

How long is COBRA coverage good for?

Typically, COBRA coverage lasts for 18 months. In some cases, like divorce or the death of the employee, it can be extended to 36 months for dependents.

Is COBRA cheaper than an ACA plan?

Often, no. ACA Marketplace plans can be significantly cheaper, especially if you qualify for subsidies. It is highly recommended to compare both options.

Future Trends and Final Thoughts

The COBRA 60-day loophole remains a vital tool for anyone navigating a job transition. While there have been temporary changes during public health emergencies, like the extended deadlines during the COVID-19 pandemic, the core 60-day rule remains a stable feature of the law.

For those considering this option, the key takeaway is to be prepared and organized. Understand your deadlines, compare your options, and have a plan for saving for the back payment if you need it.

Key Takeaways

-

The COBRA 60-day loophole lets you decide within 60 days if you want to keep your employer’s health plan, with coverage applying retroactively.

-

Use this time as a “wait-and-see” safety net. You only pay for COBRA if you need medical care.

-

You have 60 days to elect and an additional 45 days to pay the first premium, giving you up to 105 days to decide.

-

Always compare COBRA with other options like a Marketplace plan or a spouse’s plan, which can be cheaper.

-

The most common mistake is missing the 60-day deadline, which permanently forfeits your right to that COBRA coverage.

Call to Action

Navigating health insurance after a job loss can be complex and stressful. If you’re unsure whether the COBRA 60-day loophole is right for you, consulting a licensed health insurance agent can provide clarity. They can help you compare options, estimate costs, and ensure you meet all critical deadlines. Get personalized advice to make an informed decision that protects your health and your wallet.

Sources

-

U.S. Department of Labor – COBRA (General COBRA Information and Deadlines)

-

Healthcare.gov – COBRA (COBRA vs. Marketplace Plans)

-

CMS.gov – COBRA Fact Sheet (Official Guidance)

-

Proskauer Rose LLP – COBRA Election and Payment Periods (Legal Insights on COBRA)

-

Hawaii Insurance Division – COBRA FAQs (Official State Guidance)

-

Crossover – Everything You Need to Know About COBRA (Employer Perspective)

-

Taylor Benefits Insurance – COBRA Loophole 60 Days (Industry Analysis)

-

Washington Health Insurance Agency – COBRA Loophole Guide (Detailed Operational Guide)

-

Allied Benefits Solutions – Have You Heard of the “COBRA Loophole”? (Consumer-Friendly Explanation)

-

Bogleheads Forum Discussions (Real-world Experiences and Strategies)